Before you begin shopping for a house, you should

find out the maximum amount you can afford to pay. This is usually the sum of two

amounts: the cash you can offer as a down payment and amount you

can borrow.

How much can you borrow?

The first step is to shop for

a good lender. (Click

here for some excellent tips from Jack Guttentag, the Mortgage

Professor, on how to do this.) Guttentag gives top scores to

online lenders Amerisave

and E-Loan for "depth and

comprehensiveness of the information provided," so you may want

to start with them.

At either of these sites, click

"Calculators" on the toolbar, then on "How Much Can I

Borrow?" (for Amerisave) or the "Home Affordability

Calculator" (for E-Loan) to get a rough idea of what you can borrow.

In order to approve a mortgage loan, of course, a lender would need more

information about your

finances and an appraisal of the property you plan to buy.

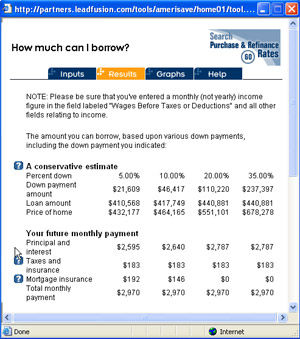

|

Many lender websites have

calculators that give you a rough estimate of how much you can

borrow. |

How much should you borrow?

You'll probably be pleasantly

surprised at the amount of money you'll be able to borrow--loan

officers can stretch you to the limit (and beyond) of your ability to

pay with creative devices like adjustable rate mortgages (ARMs),

graduated mortgages, and

interest-only loans. But before you start house hunting, you

should think carefully about how much you should borrow.

Here's a good

resource for thinking this through.

Be aware that mortgage loans over

$417,000 are called jumbos or conforming jumbos (sometimes called

confumbos) and carry higher interest rates than those

under $417,000, which are called conforming or conventional loans.

If possible, try to keep your borrowing below that threshold.

See if you can improve your credit score

Your credit report gives the lending

industry's assessment of how good a credit risk you are. Since this

is one of the factors that a lender considers before approving a

loan, you'll want your score to be as high as possible.

The government requires credit

reporting companies to give you a free annual credit report. Make

sure you go to

annualcreditreport.com to get it. (This

government website explains why you should avoid all the imposter

websites that also offer free credit reports.)

It's a good idea to check your score

early on, so you'll have time to improve it by

fixing errors or making changes in your finances. This

CNN Money article offers suggestions on how to improve your

score.

Pre-approval

When considering offers, sellers

don't just look at price. They also care about whether the deal

is likely to make it through escrow. Sellers hate it when deals

fall through.

A relatively painless way to sweeten

your offer is to append a pre-approval letter or certificate to

it. The letter says that the bank has reviewed your financial

information and that it's willing to lend you enough money to buy the

house at the price you've offered, assuming other conditions are met. It

won't show the maximum

amount you can borrow, though, since that would tip your hand to the

sellers.

Getting pre-approved takes just a day

or so, and involves filling out an application and submitting

documents like paycheck stubs and bank statements. You shouldn't

have to pay a fee.

|

Applying for a loan is no

longer an ordeal, since lenders have access to an alarming

amount of information about you. |

Pre-qualification is similar to

pre-approval, except that the

financial information provided by the buyer isn't verified.

Because of this, a pre-qualification letter won't impress sellers as

much as a pre-approval letter. (Click

here to read more about the differences between pre-qualification and pre-approval.)

|

People will often spend

more time shopping for shoes than they will a loan. But

shopping for a slightly lower interest rate can save you lots of money over

time. |

Next topic: Shopping

©Lori

Alden, 2008. All rights reserved.

|